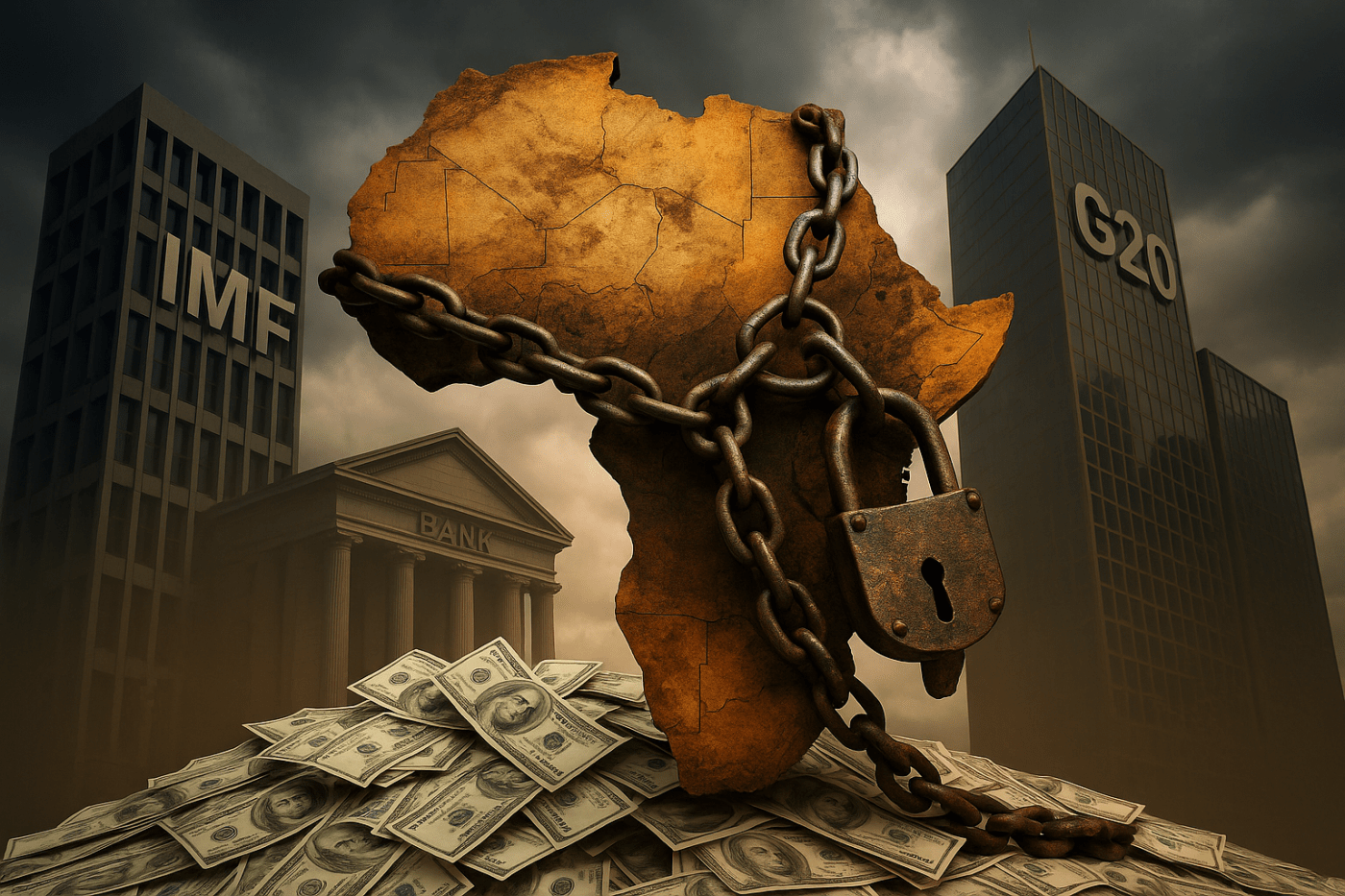

Africa’s $1.8 trillion debt crisis is not a financial accident—it is the product of centuries of plunder, ongoing extraction, and a global order built to keep the continent subordinate. This article excavates the propaganda, exposes the buried facts, and reframes Africa not as a debtor in distress but as a frontline in the global struggle for sovereignty and multipolar liberation.

By Prince Kapone | Weaponized Information | November 13, 2025

How to Tell a Story Without Telling the Story

The Business Insider Africa article, “Africa’s debt reaches $1.8 trillion as AU cries for global financial reform”, arrives dressed in the neutral, technocratic tone that global financial journalism wears to work. On its surface, it simply reports that Africa’s total public debt has swelled, that the African Union is appealing to the G20 for reforms, and that the global financial architecture may need some updating. It reads like a weather report for the indebted: the clouds are gathering, the winds are shifting, and someone somewhere ought to bring an umbrella. But as with all imperial news, the rain is never falling from the sky—someone’s always standing over the continent with a bucket.

The article is penned by Segun Adeyemi of Business Insider Africa, the African outpost of one of the world’s major business media franchises. As with its parent institutions, the outlet’s primary audience is investors, corporate managers, and the policy class that services them. Its ideology is not declared but embedded: a worldview where capital is the measure of civilization, where indebted nations are guilty until proven solvent, and where structural crises appear by acts of God rather than design. Adeyemi’s role—through training, institutional expectations, and audience demands—is to translate global financial power into digestible language, to describe the architecture of domination without ever naming the architects.

And so the article begins with a familiar performance: Africa is cast as a singular, suffering body, its “debt burden ballooning,” its governments spending too much on “servicing,” its leaders crying for reform. This one-size-fits-all Africa—a continent flattened into a metaphor—appears throughout the piece, an indebted monolith rather than the home of fifty-four distinct nations, each with its own economy, history, and struggle. In this narrative, Africa does not act; it reacts. It does not decide; it pleads. A continent is transformed into a patient lying on the floor of a global clinic, waiting for the G20 to check its vital signs.

The propaganda work here is not done with loud declarations but with quiet omissions. The story is full of urgency but empty of agents. Debt “balloons,” “mounts,” and “spirals” on its own, like a natural disaster. Africa’s social spending is crowded out by “debt servicing,” yet no creditor is named, no institution implicated, no mechanism examined. The reader is guided through a room full of smoke but never shown the fire. This is the subtle art of crisis without perpetrators, suffering without cause—an imperial narrative specialty.

Likewise, the article uses a classic ventriloquism device: the only voices allowed to speak are AU officials carefully framed within the discourse of global finance. They lament inequality in the system but stop short of naming the system’s beneficiaries; they call for reform, not rupture. Their voices, filtered through the outlet, are made to appear as self-evident truth, as though all African political imagination has been condensed into polite appeals for a slightly fairer version of the same centuries-old arrangement.

Then comes the soft power bait-and-switch. The G20—an exclusive club dominated by the very creditors and imperial powers that shaped Africa’s economic position—is framed as a benevolent actor. The article suggests that under South Africa’s presidency, the G20 is listening, opening doors, creating “expert panels,” granting Africa a “stronger voice.” In the imperial household, this is called being allowed into the foyer while the real conversations happen behind closed doors. But the narrative framing is meticulous: the G20 is not portrayed as the superintendent of the crisis, but as the sympathetic landlord checking in on a distressed tenant.

Perhaps the most consequential propaganda device is what the piece consistently refuses to say. It never asks who Africa owes. It never inquires about the conditions attached to those loans. It never examines how interest rates, credit ratings, currency asymmetries, or decades of externally imposed “reforms” engineered this crisis. It never touches the colonial history that birthed the modern debt regime. These omissions are not mistakes; they are the architecture of the article. They function as a soft, managerial ideology: accept the crisis, accept the debt, accept the rules; the only thing negotiable is how politely Africa may ask for relief.

In the end, what the article delivers is not information but a worldview. It instructs the reader to see Africa through investor eyes: as a ledger, a risk profile, a body of liabilities. It shows us a continent crying out for reform while concealing the forces that produced the cry. It reduces structural violence to financial weather, and political struggle to fiscal housekeeping. And in doing so, it tells a story without telling the story—leaving us to excavate the truth buried beneath its polite, technocratic rubble.

The Numbers Behind the Silence: What the Article Hides About Debt, Power, Plunder, and the Drain of African Wealth

The Business Insider Africa article gives us a handful of polished facts—$1.8 trillion in total public debt, $70 billion in annual servicing, debt-consuming social budgets, and AU appeals for G20 reforms—but it offers them without roots, without lineage, and without the political economy that gives these numbers meaning. Before we can reframe the narrative, we must first reconstruct the terrain the article leaves unspoken: the historical forces that produced Africa’s debt, the global structures that maintain it, and the vast architecture of extraction that turns the continent’s labor and resources into revenue for institutions far beyond its shores. Section I dissected the propaganda techniques; here, we examine the material world they obscure.

Africa’s debt crisis cannot be understood without acknowledging a foundational truth: across the Global South — including many African countries — governments have already repaid more in debt service than they originally borrowed, with Jubilee researchers noting that developing countries have already paid back more than the original loan amounts and Catholic/Jubilee analysts confirming that many nations have repaid the principal several times over yet remain in crisis because interest continues to grow. They remain trapped in debt because of soaring interest payments, runaway interest accumulation, currency depreciation driven by dollar-denominated borrowing, and refinancing cycles that keep them on what researchers describe as a debt treadmill stretching back to the 1980s. A loan that may have been a few hundred million dollars decades ago has, through compounding interest and exchange-rate shocks, swollen into multibillion-dollar obligations, a dynamic reflected in the fact that developing-country debt stocks have grown to nearly four times their 1980 levels despite continuous repayment and that many nations now experience negative net transfers, paying back more than they receive. This reality alone would destabilize the news article’s narrative of African indebtedness as a matter of fiscal mismanagement or unfortunate circumstance. But this truth is not mentioned.

Even less mentioned is who Africa actually owes. Western private creditors—such as Eurobond holders, hedge funds, and major banks—account for a large and growing portion of Africa’s external debt. These actors often refuse to participate in restructuring processes. They demand full repayment even when the debts are unpayable without cutting social services, firing public workers, or privatizing essential infrastructure. Their power is amplified by Western credit-rating agencies—Moody’s, Standard & Poor’s, and Fitch—whose downgrades can raise borrowing costs overnight. These downgrades often have little to do with the underlying health of African economies and everything to do with investor risk perceptions shaped by systemic bias, with an IMF working paper finding a 2.9-percentage-point “risk premium” imposed on African issuers beyond economic fundamentals. The article does not mention any of this.

Nor does it confront the central role of U.S. and European monetary policy. When the U.S. Federal Reserve raises interest rates, African countries that borrow in dollars instantly see their debt burdens rise. Their currencies fall, inflation rises, and repayment costs surge, with analysts showing that African currencies lost around 8% of their value during periods of U.S. rate-hiking, increasing debt burdens by nearly 10% of GDP in some countries according to ONE’s analysis. A decision made in Washington, meant to stabilize U.S. markets, becomes an economic crisis in Lusaka, Accra, or Nairobi. This mechanism—identified by African policy researchers as a key driver of worsening debt conditions in the region through borrowing-cost amplification—is one of the primary engines of Africa’s present debt spiral. It is wholly absent from the article.

A deeper omission concerns the role of the multipolar world, especially China and Russia. China has provided hundreds of billions in infrastructure loans across Africa, often at below-market interest rates, and has repeatedly forgiven interest-free loans and restructured debts for African countries facing repayment challenges. Contrary to the “debt-trap diplomacy” narrative, China typically avoids imposing austerity or privatization conditions; instead, it finances railways, ports, power plants, and telecommunications networks—the kinds of long-term development investments Western creditors abandoned decades ago. Russia, meanwhile, has forgiven more than $20 billion in African debt inherited from the Soviet era and has cancelled or restructured additional obligations in recent years. It also provides agricultural, energy, and security cooperation that gives African states alternatives to Western-controlled markets. None of these multipolar relationships appear in the article because acknowledging them would destabilize the myth that Western financial institutions are Africa’s only path to development.

Yet even these dynamics are only part of the story. Africa’s debt crisis sits atop a far older and more violent history of wealth extraction. For centuries, Africa was plundered through the transatlantic slave trade, colonial occupation, forced labor, and resource theft. Trillions of dollars’ worth of gold, diamonds, rubber, oil, copper, cocoa, timber, and uranium flowed out of Africa into the treasuries and industries of Europe and the United States, and global studies of value transfers show persistent, large-scale extraction from African economies to the Global North through unequal exchange and imperial appropriation. Entire nations were impoverished so that European states could industrialize. No serious analysis disputes that the world continues to extract billions annually from African resources, and no honest discussion of Africa’s contemporary debt can be separated from the colonial plunder that enabled the rise of Western power.

More than historical memory, this extraction continues today through unequal exchange. Multinational corporations use transfer pricing and profit shifting to drain billions from African economies every year. They underprice African exports, overprice imports, and move profits through tax havens. The African Union’s High-Level Panel on Illicit Financial Flows and the United Nations–commissioned research have documented tens of billions of dollars lost annually through illicit financial flows—money that exceeds all development aid and foreign investment in many years. Commodity prices are determined not in African capitals but in London and New York, shaping terms of trade that systematically benefit Western corporations and disadvantage African producers. When Africa exports raw materials at low prices and imports finished goods at high prices, the drain of wealth becomes structural rather than incidental.

Add the colonial currency regimes, such as the CFA franc, which ties 14 African nations to French monetary oversight, requiring them to hold a portion of their foreign reserves in the French Treasury. Add the impact of global commodity price shocks that are shaped by speculative markets far removed from African production. Add the austerity measures and privatization mandates imposed through IMF and World Bank Structural Adjustment Programs. Add the fact that when all outflows are accounted for—debt service, profit repatriation, illicit flows, and unequal exchange—Africa becomes a net creditor to the world. The continent sends out far more wealth than it receives, as shown by long-term capital flight estimates documenting more than US$1.4 trillion drained from Africa through trade misinvoicing and illicit financial flows.

When Business Insider Africa notes that Africa’s debt service exceeds its social spending, it inadvertently gestures toward this broader story without naming it. The AU’s warnings become clearer when situated within this historical and geopolitical terrain: Africa’s debt is not a natural accumulation of fiscal errors but the product of a global financial order that positions African nations as perpetual debtors, even when they are structurally exploited creditors. The G20’s gestures of inclusion do not change the fact that Western states and private creditors continue to shape the rules of the system while South–South alternatives struggle for space in a world dominated by the dollar.

To extract these omitted facts is not to editorialize; it is to reconstruct reality. Africa’s debt crisis is not a story of numbers rising and falling in a vacuum. It is the outcome of centuries of plunder, decades of conditionality, and ongoing mechanisms of unequal exchange that drain Africa’s wealth into the coffers of the same countries that now pose as guardians of fiscal stability. Only by acknowledging this full context can we understand the significance of the AU’s call for change and the broader geopolitical struggle that surrounds it. The facts omitted by the article expose what the article seeks to avoid: that Africa’s debt crisis is not a financial anomaly but a structural feature of the imperial world economy.

The World Turned Upside Down: Reframing Africa’s Debt Through the Lens of Extraction, Sovereignty, and Class Struggle

Once we gather the full weight of the omitted facts—the repaid principals that somehow remain unpaid, the private creditors who refuse restructuring, the interest rate shocks exported from Washington, the multipolar lifelines ignored by Western media, the trillions looted through colonial plunder, and the ongoing hemorrhage of wealth through unequal exchange—a different narrative emerges. It is not the narrative of an indebted continent crying out for reform, as Business Insider Africa presents it. It is the narrative of a continent ensnared in a global economic order designed to extract far more than it ever gives, and punished whenever it attempts to break free. The debt that Africa “owes” turns out to be a political fiction built atop historical theft and contemporary exploitation. The real debt is owed in the opposite direction.

To make sense of this reversal, we need a framework rooted not in the polite language of international finance but in the lived realities of the working classes, peasants, and oppressed nations whose lives are shaped by decisions made in boardrooms, central banks, and creditor courts. Africa’s debt crisis is best understood not as the failure of African governments to manage their finances, but as the deliberate success of an imperial system whose purpose is to maintain Africa’s subordination. Debt is not merely a number on a spreadsheet—it is a weapon. It disciplines states, constrains budgets, and forces political compliance. It is the modern successor to colonial rule, a form of control that extracts resources without requiring a single soldier on the ground.

Viewed through this lens, the AU’s call for reforms is not just bureaucratic complaint—it is an expression of a deep structural contradiction. African nations operate in a system where they have already repaid what they borrowed, yet remain perpetually indebted because the rules ensure that repayment never ends. They borrow to build infrastructure, but the value created by that infrastructure is siphoned away through transfer pricing and profit repatriation. They borrow to stabilize their currencies, but global interest rate decisions destabilize those currencies even more. They borrow to weather external shocks, but those shocks are often created by the very financial powers that later demand repayment. This is not mismanagement; it is entrapment.

The deeper contradiction is temporal. Africa’s current debt is presented as a contemporary fiscal concern, but it is inseparable from five centuries of extraction. When Europe forcibly removed millions of Africans, looted mineral wealth, seized land, expropriated labor, and imposed currency regimes that still exist today, it created the material basis of Western modernity. The accumulated value of this theft—measured not only in resources but in human lives, stolen futures, and destroyed economic systems—is immeasurable. And yet Africa is framed as the debtor. This inversion is not just ideological—it is foundational to the functioning of global capitalism. The world system needs Africa to be poor, indebted, and dependent so that capital may continue to flow outward.

But the story does not end with extraction. Something new is taking shape. Africa’s increasing engagement with China, Russia, and the broader multipolar world is not a matter of diplomatic convenience—it is an act of strategic survival. Chinese debt forgiveness, infrastructure financing, and restructuring practices undermine the idea that Africa’s only options are Western lenders who impose austerity as the price of development. Russia’s cancellation of Soviet-era debts and its expanding agricultural, energy, and security partnerships signal another model of cooperation that does not rely on the coercive instruments of the IMF and World Bank. South–South institutions like BRICS, the New Development Bank, PAPSS, and the push for an African Monetary Fund represent early steps toward a new financial architecture. These initiatives are uneven, imperfect, and contradictory, but they embody the possibility of escaping the Western-controlled system.

From the standpoint of the global working class and the colonized nations, these shifts are neither marginal nor symbolic. They represent cracks in the foundation of the hyper-extractive world order. Africa is not simply seeking better loan terms—it is seeking sovereignty over its development path. That sovereignty threatens the existing hierarchy of global capitalism. A continent that keeps more of its mineral wealth, that negotiates its own terms of trade, that refuses austerity, that builds infrastructure without Western oversight—that continent represents a material threat to the ruling class interests of the imperial core. Thus, the debt narrative, as produced by outlets like Business Insider, functions as ideological maintenance. It obscures the historical theft, the ongoing drain of value, and the emergence of alternatives by focusing narrowly on numbers divorced from their political meaning.

To reframe the story is to place Africa not as a failing debtor but as a central battleground in the global struggle for economic sovereignty. It is to see debt as an instrument of counterinsurgency deployed against nations that dare to imagine a future beyond dependency. It is to understand that Africa’s call for a new financial architecture aligns with broader proletarian and peasant struggles across Latin America, Asia, and the Middle East. It is to recognize that the fight over Africa’s debt is part of a much larger confrontation between an aging imperial order and a rising multipolar project seeking to build a world not organized around extraction.

And from this reframed standpoint, the contradictions sharpen. The imperial core insists Africa must continue paying its debts, even though Western nations built their wealth through centuries of theft. The AU declares the global financial system obsolete, yet must negotiate with creditors who benefit from the system’s continuation. Multipolar partners offer alternatives, yet Africa remains constrained by dollar dominance and punitive ratings. The global working class sees its own struggles reflected in Africa’s condition—wage theft, austerity, privatization, inflation—because the same capitalist logic governs their lives.

What emerges is a clear dialectical truth: Africa is not in debt because it has borrowed too much; Africa is in debt because the world economy requires it to be. And the rising movements toward multipolarity, development sovereignty, and regional financial autonomy are not merely reactions—they are beginnings. They are the first steps in a global struggle to overturn a system that extracts from the many to enrich the few. Africa’s debt crisis is not the end of the story. It is the opening chapter in a new fight for liberation.

Turning the Page: The Struggle for Debt Liberation Is Already Underway

If Africa’s debt crisis reveals the architecture of global financial domination, it also reveals the contours of the struggle against it. Throughout the continent and across the diaspora, movements, unions, networks, and grassroots organizations are fighting—not in the realm of soundbites and polite appeals, but through campaigns that challenge the very foundations of the system that Business Insider Africa describes as if it were natural law. The story of Africa’s debt is a story of extraction, but the story of Africa’s people is one of resistance. Section after section of the continent has refused to accept austerity as destiny. Across the imperial core, allied forces are pushing back against the institutions that profit from Africa’s subordination. The mobilization is not theoretical; it is material, organized, and already in motion.

On the continent, the most consistent voices in this struggle include the African Forum and Network on Debt and Development (AFRODAD), which for decades has documented the human cost of debt servicing and demanded public, transparent negotiations that prioritize social needs over creditor profits. CADTM—the Committee for the Abolition of Illegitimate Debt—works with African partners to challenge the legal and moral legitimacy of debts imposed under conditions of coercion, corruption, or structural violence. In Kenya, popular resistance to the 2023–2024 tax hikes and IMF-driven austerity has erupted into mass protests, particularly among working-class youth, forcing the government into partial retreats. In Ghana, movements such as the Economic Fighters League have exposed how debt and IMF conditionalities have hollowed out public services. In Nigeria, trade unions and student movements continue to fight against the privatization of education, fuel subsidies, and currency devaluation measures linked to external financial pressures.

Across the Global South, new forms of financial cooperation are emerging as expressions of sovereign will: BRICS+ development pathways, the push for an African Monetary Fund, regional payment systems designed to bypass the dollar, and South–South investment platforms that seek to break the chokehold of Western financial institutions. These initiatives, whatever their contradictions, represent an expanding political horizon in which African states and peoples assert the right to develop on their own terms. The struggle for financial sovereignty is not confined to conference halls—it is alive in the streets, in union halls, in community assemblies, and in the daily fight to resist austerity measures imposed from abroad.

In the imperial core, solidarity means more than abstract declarations. Organizations such as Debt Justice (formerly Jubilee Debt Campaign) in the UK, Black Lives Matter’s global solidarity networks, progressive diaspora groups in Europe and the United States, and radical student organizations have taken up the fight against creditor power by exposing bond market profiteering, challenging credit rating agency manipulation, and connecting local austerity struggles to those unfolding across Africa. Palestinian solidarity networks, climate justice movements, and anti-imperialist formations have begun linking their work to the campaign for global debt justice, recognizing that the same institutions driving African austerity also finance settler colonialism, fossil fuel extraction, and militarized policing.

For revolutionaries in the Global North, the path forward requires anchoring our struggle in these living movements rather than inventing new ones. We can help build a unified front that challenges the institutions most responsible for Africa’s debt crisis: the IMF, the World Bank, credit rating agencies like Moody’s and Standard & Poor’s, hedge funds holding African sovereign bonds, and multinational banks that profit from billions in interest payments. This means supporting campaigns for total debt cancellation; pushing unions, universities, and public pension funds to divest from African sovereign bonds that fuel austerity; building public dossiers on creditors that refuse restructuring; expanding diaspora-led pressure campaigns against IMF conditionalities; and creating digital counter-mapping projects that expose how wealth flows from African workers to Western financial centers.

But the work must also be intimate: forming study groups that connect local struggles against evictions, student debt, wage theft, and privatization to the broader terrain of international financial oppression; building popular assemblies that include African diaspora communities and grassroots groups on the continent; creating militant internationalist political education programs that treat Africa’s financial liberation as part of our own liberation. We cannot fight the global financial order piecemeal. We must connect the struggle for African sovereignty to the struggles of workers in Detroit, students in London, tenants in Berlin, and migrants in Paris who confront the same system in different forms.

The global working class and the colonized nations do not stand at the edge of a crisis—they stand at the edge of a rupture. The financial system described in the Business Insider article is cracking under the weight of its own contradictions, and new forms of political possibility are emerging. The question is whether we will treat Africa’s debt crisis as a spectacle to observe or as a battle to join. Every movement named above, every protest, every campaign, every act of resistance is already pointing the way. The task now is to deepen these struggles, connect them, and expand them until Africa’s demand for financial sovereignty becomes part of a broader global movement for justice. The liberation of Africa is not the endpoint—it is a crossroads. And the struggle for that liberation is a struggle that belongs to all of us.

Leave a comment