The Economist’s 2026 outlook presents a world of “manageable risks” and “resilient markets,” but behind the technocratic polish lies a deeper reality: an imperial economy held together by tariffs, debt, financial coercion, and speculative bubbles, whose costs are offloaded onto workers and the Global South. This essay excavates the propaganda, exposes the suppressed material foundations, and reframes the coming year as a phase in the long crisis of Western hegemony and the sharpening struggle over the multipolar future.

By Prince Kapone | Weaponized Information | November 18, 2025

Rolling With the Punches for Whom?

The latest sermon from the priesthood of capital comes dressed up as a sober forecast for the year ahead. In his piece, “Expect mediocre growth and, in America, too much inflation in the year ahead”, Henry Curr, economics editor at The Economist, tells us that the world economy has “rolled with the punches.” The pandemic came and went, interest rates shot up, Trump’s “Liberation Day” tariffs scared the markets—and yet, we are assured, there was no great collapse. Growth slowed but did not die. Now, we are told, 2026 will be a year of “mediocre” expansion and stubborn inflation in the United States, haunted by tariffs, deficits, nervous bond markets and the possibility that the AI stock boom might turn back into a pumpkin at midnight.

It sounds almost reasonable, like a doctor calmly explaining the vital signs. But the first task in any serious excavation of propaganda is to ask: whose world is being measured, and whose punches are we talking about? When The Economist says the global economy has “rolled with the punches,” it does not mean the garment worker on half-wages, the delivery driver juggling three jobs, or the farmer priced out of fertilizer and fuel. It means that the institutions of capitalist rule—central banks, bond markets, multinationals—have survived each crisis without being forced to surrender power. The article reads like a victory lap written in the key of anxiety: the system is still standing, but the managers are sweating.

Look at who is speaking. Henry Curr is not some neutral observer in the rafters. He is the model product of the Anglo-American economic priesthood: elite schooling, think-tank circuits, rapid ascent inside the house journal of global business, the go-to voice on inflation, interest rates and debt for investors, policymakers and talking heads. His job is not to understand the world for the poor. His job is to make the storms of capitalism sound like weather patterns—unavoidable, regrettable, but ultimately manageable by the right sort of grown-ups.

And then there is the pulpit he stands on. The Economist is not just another newspaper. It is the weekly instruction manual of the transatlantic ruling class, owned and overseen by a web of old money families and financial interests whose fortunes are tied to the smooth functioning of this system. For nearly two centuries it has preached the same gospel: free trade for corporations, discipline for workers, “sound money” for creditors, and war when “markets” require it. When it publishes its “World Ahead” special, it is not chatting with you at the bus stop. It is briefing ministers, central bankers, CEOs and hedge funds on how to think about the coming year.

Notice who appears in Curr’s story and who does not. The central characters are President Trump, the Federal Reserve, the Supreme Court, bond traders, AI investors, and the “markets” as a kind of temperamental deity. The supporting cast are the governments of France, Britain and Japan, whose fiscal headaches and fragile bond markets are presented as possible epicentres of the next panic. Missing entirely are the workers in those countries whose wages, pensions and public services are carved up every time the bond market throws a tantrum. Disappeared, too, are the billions in the Global South whose economies are already being sacrificed to keep this sluggish world order “resilient.”

The text leans on a set of familiar tricks. Trump’s tariff offensive is rechristened “Liberation Day,” as if the purpose was to free American workers rather than to reshuffle profits between factions of capital and weaponise trade against rivals. The watering down of his initial tariff scare becomes proof of market wisdom and institutional stability, not evidence of chaotic, corporate-driven policymaking. Public debt is treated as a kind of unfortunate hangover from pandemic stimulus, not as the bill from decades of tax cuts for the rich, endless war spending, and the socialisation of private losses after each crisis. Central bank “independence” is presented as a sacred, neutral principle under threat from Trump’s ego, not as a political arrangement that has long put the security of creditors above the lives of workers.

Even the danger scenarios are framed in class shorthand. A bond-market crash is described as a threat to “global financial conditions,” not as the trigger for another round of austerity, layoffs and privatisation imposed on real people. A collapse in AI stock prices is discussed mainly as a hit to household “wealth effects,” as if the main consequence of this boom and bust were some unhappy brokerage accounts rather than a round of job cuts, intensified surveillance and shattered retirement dreams. The text never names who owns the AI boom, who labours in the data mines behind it, or who will pay the price if the bubble bursts.

All of this is why we begin with excavation and not with debate over numbers. At this stage we do not try to correct Curr’s statistics or substitute better forecasts. We map the ideological architecture. We mark how an imperial outlet packages a set of very real dangers—tariffs, debt, fragile bond markets, speculative manias—into a story that keeps power where it is. We note how the author personalises structural problems into a soap opera about Jerome Powell’s successor, how he turns the class politics of monetary policy into a matter of “credibility,” and how he treats the lives of ordinary people as background noise to the drama of markets.

Once the spell is named, it begins to lose its power. The point of this first step is simple: before we can extract facts or build our own analysis, we have to see clearly what this article is doing. It is not a neutral weather report. It is a message from the managers of a tottering system to one another, rehearsing their fears and rehearsing their solutions. Our task, as weaponized readers, is to flip the script—and that begins by understanding exactly how it has been written.

What the Numbers Say—and What They’re Forced to Hide

When you strip away the editorial perfumes and capital-class anxieties of The Economist, you’re left with a handful of hard data points arranged like ornaments on a tree whose roots we’re never permitted to see. Thus we must pull those ornaments down, lay them on the table, and reconstruct the world they actually belong to. Not the world as narrated by Wall Street wolves and the banksters, but the world as lived by workers, farmers, debtors, and entire societies squeezed between tariffs, interest rates, and the volatile whims of AI speculation.

Begin with the numbers Curr puts forward. They seem straightforward: the average U.S. tariff rate sits a little above 10%; the Fed expects Trump’s tariffs to add roughly one full percentage point to inflation by spring; America’s fiscal deficit is projected to be around 6% of GDP; France and Britain face “parlous” public finances; and global markets remain fragile enough that a deeper shock—perhaps triggered by an AI bust or a bond panic—could tighten credit worldwide. He points to the Fed succession battle, the legal fight over Lisa Cook’s removal, Japan’s soaring debt burden, Britain’s 2022 gilt meltdown, and the possibility that inflated AI valuations are propping up American consumption more than real economic strength is. None of these claims are invented. None need to be dismissed. The problem is not the numbers—it is the universe they are made to orbit.

Because what The Economist offers is not a factual baseline but a curated slice of reality, trimmed to reinforce elite priorities. The article counts tariffs but not their global spillover: evidence shows that tariff increases impose large costs on consumers and disrupt supply chains for global producers. Tariffs may reduce potential output by disrupting global supply chains. It acknowledges inflation but buries who pays it. It notes deficits but never the trillions shoveled upward through tax cuts, corporate subsidies, and military budgets: U.S. corporate tax breaks alone reached about $1.9 trillion in 2024, and increased military spending without offsetting revenue risks tripling the fiscal gap. Proposed defense spending increases would more than triple the fiscal gap. It gestures at stock-market “wealth effects” while omitting the simple fact that most people own little or no stock: as of 2022, only about 58 % of U.S. families owned stocks directly or indirectly, and ownership is highly skewed toward the wealthiest. It warns of bond-market fragility but leaves aside the deeper structure of global debt, where the periphery is already buckling under interest-rate hikes. Rising interest rates are driving growing debt burdens in low- and middle-income countries. In other words, the article counts what matters to capital and omits what matters to everyone else.

So what does a fuller picture look like? First, tariffs are not a local inflation problem—they are a global tax on workers. Every country tied to U.S. supply chains pays through higher prices, disrupted employment, and lost export revenue. New U.S. tariffs show consumer-goods prices rising and supply-chain disruption and Chinese firms cutting pay and jobs amid U.S. tariffs. The “trade war” is not simply Trump’s personal indulgence; it is the economic arm of an empire trying to claw back advantage in a multipolar world. Second, global debt is not an unfortunate legacy of pandemic stimulus—it is a systemic feature of an economic order that offloads the costs of crisis onto public budgets while profits flow upward. Global public debt hit record US$102 trillion in 2024, developing countries especially burdened. European deficits are not random policy failures; they are the accumulated residue of neoliberal governance. Neoliberalism dominant in European crisis-resolution and budget consolidation. Japan’s towering debt ratio cannot be understood without understanding decades of stagnation and corporate hoarding. Japan’s government debt rose from ~70% of GDP in 1998 to ~195% in 2023 amid stagnation. And the U.S. deficit, with or without tariff revenue, reflects an economy whose ruling class refuses to pay for the infrastructure, climate transition, and social supports it depends on.

Third, bond-market fragility is not a ghost from Britain’s past—it is the nervous system of global finance. The UK “mini-budget” crisis exposed how thin the ice has become: a small policy shock triggered a chain reaction among leveraged funds, nearly collapsing the pensions of millions. UK pension funds were highly vulnerable to sharp gilt-yield changes and liability-driven investment positions triggered a bond market meltdown after the 2022 mini-budget. France and Japan face similar stress points. France is under bond-market pressure amid fiscal and political instability and Japan’s high public debt and weak bond-market structure raise global alarm. In the U.S., the bond market is a monster whose appetite determines the spending priorities of the state: schools can be cut, health care can be slashed, but the bondholder must be fed. Global bond markets remain fragile and set the conditions for state spending. The Economist nods to this danger but refuses to name its real implication: democratic institutions, such as they are, operate under the permanent threat of financial reprisal.

Fourth, the AI boom is not a broad-based engine of growth—it is a thin, precarious layer of speculative capital concentrated in a handful of mega-firms. Large investments, few clear returns show that infrastructure spending by a small elite is outpacing actual revenue across the AI ecosystem. Most companies experimenting with AI have yet to see profits. Analysis by Wired reports many major AI players are burning billions and not delivering commensurate earnings. Most workers see only surveillance and job precarity, not opportunity: The National Employment Law Project documents how AI-enabled surveillance tools increase precarity rather than deliver widespread worker empowerment. Those “wealth effects” driving consumption exist almost entirely for the richest 10 % of households: Stock-ownership concentration data show the richest decile of U.S. households hold the vast majority of market wealth. A collapse in AI stocks would not simply “reduce confidence”—it would expose how artificial, how engineered, the supposed resilience of the U.S. economy has been. The European Central Bank warning of an AI-stock bubble.

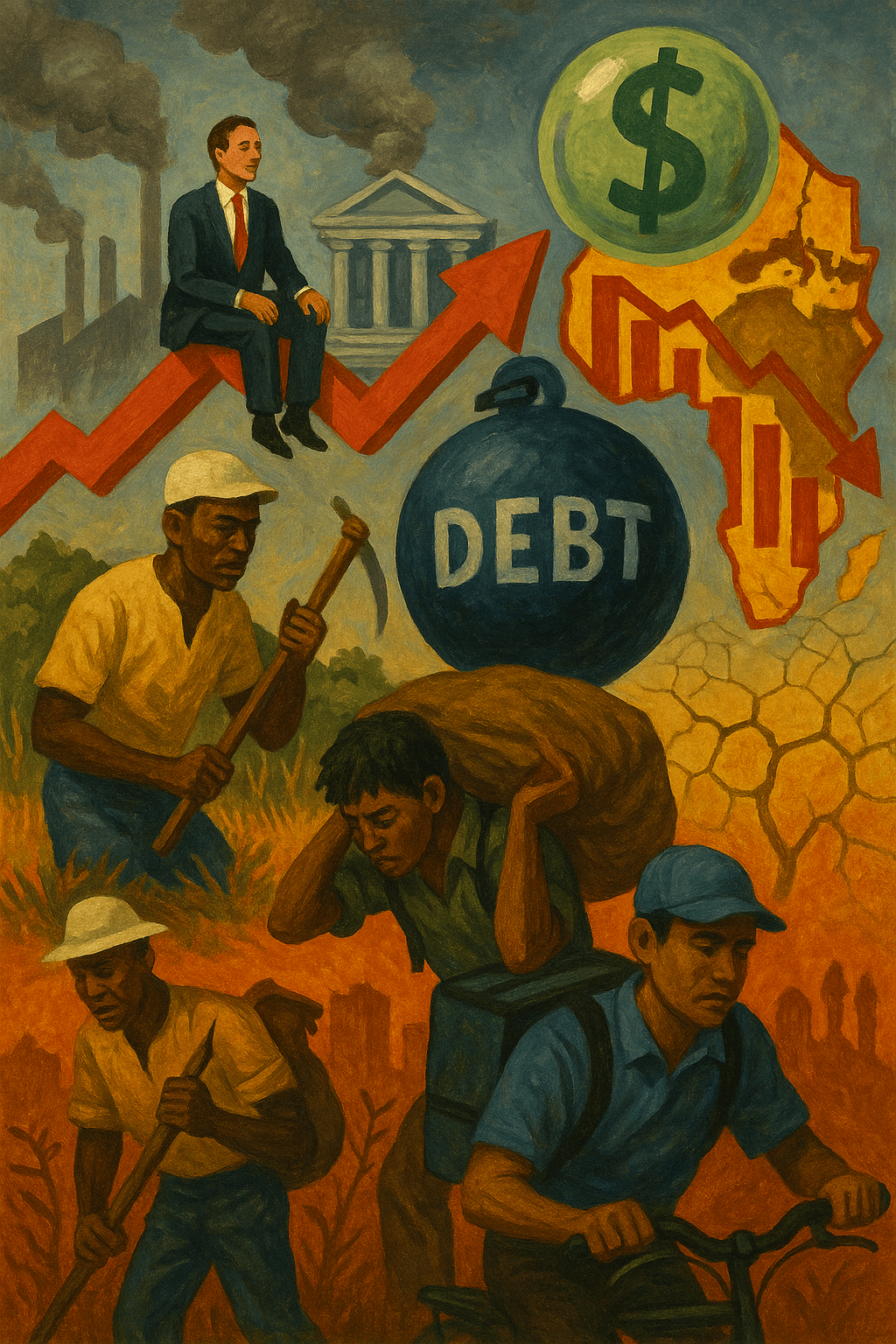

Finally, perhaps the most decisive omission: the Global South. You could read Curr’s article and imagine a world economy made up only of North America, Western Europe, and Japan. No mention of the debt crises wracking dozens of African nations. Many African countries are currently in fiscal and debt crises. No mention of Latin America’s struggle against IMF austerity. The IMF and class struggle in Latin America documents how austerity is imposed via debt regimes. No mention of West Asian economies staggering under sanctions or climate shocks. Developing countries (including West Asia) face rising debt burdens that impede climate and development goals. No mention of the BRICS+ economies or their attempts to build new financial structures outside the dollar system. Research on de-dollarisation and BRICS+ alternative financial structures. The Economist pretends these forces do not exist, even as they increasingly shape the terrain of world politics and economics.

That is the core of this section: to establish the factual terrain in its fullness, without the blind spots engineered into the original narrative. The data The Economist uses is not wrong—it is incomplete by design. It is architecture without foundations. It is a map that includes the roads used by bankers but erases the homes of workers, the farms of the South, and the factories of the East. By bringing the omitted realities back into the frame, we prepare the ground for what comes next: a reframing that reveals how these numbers fit into a global system in crisis, and why the ruling class clings to these narratives to maintain command over a world slipping from its grasp.

When a System Manages Crisis by Expanding It

Now that the facts and omissions sit side by side, the silhouette of the real story comes into view. What The Economist describes as a series of unfortunate headwinds—tariffs nudging inflation up, deficits raising eyebrows, bond markets twitching, AI valuations wobbling—is not a scattered cluster of risks. It is the operating logic of a world order trying to outrun its own contradictions. A system that cannot produce stable growth must instead produce new fronts of crisis. A system that cannot deepen legitimacy must deepen discipline. And a system in decline must force someone else to absorb the shock. This is not turbulence. It is strategy.

At the heart of this strategy sits monopoly finance capital, the stage of capitalism where profits no longer come from production but from leverage, rents, asset inflation, and the engineered scarcity that feeds them. The Economist never uses the term, but the entire architecture of its forecast depends on it. Bond markets dictate fiscal policy. Central banks calibrate wages and unemployment like a thermostat. Asset bubbles—whether in AI, tech, or real estate—are treated as indicators of “resilience” rather than danger. The U.S. cannot generate real growth, so it manufactures paper wealth; Europe cannot stabilize wages, so it disciplines public budgets; Japan cannot escape stagnation, so it hoards liquidity. These are not policy failures—they are the mechanisms through which monopoly finance capital keeps itself alive by siphoning value upward while hollowing out society beneath it.

Seen through this lens, Trump’s tariffs are not rogue improvisations but the blunt weapon of a ruling class increasingly defined by factional conflict. This is where the Yankee–Cowboy–Digerati paradigm becomes indispensable for understanding the political economy beneath the economist’s prose. Trump’s tariff war is Cowboy economics: coercive, chaotic, unilateral, driven by the settler frontier ethos of confrontation. The Federal Reserve’s interest-rate choreography and the bond market’s punitive discipline are classic Yankee instruments: financial supremacy, institutional control, the management of crisis through austerity and credit. Meanwhile, the speculative AI boom—so central to The Economist’s narrative—is the preferred terrain of the Digerati: Silicon Valley monopolists whose data extraction, surveillance systems, and financialized valuations offer the illusion of vitality while masking the system’s rot. Together these factions do not represent competing alternatives but complementary weapons in the management of imperial decline.

This dynamic does not operate in a vacuum. It flows directly from the long arc of trilateral imperialism—the imperialist triad of the United States, Western Europe, and Japan—whose dominance shaped the world for nearly half a century. But the triad is no longer ascending. Its members are debt-heavy, politically unstable, and increasingly reliant on coercive mechanisms rather than productive leadership. The Economist’s narrative pretends these powers still form the gravitational center of global accumulation, yet everything in the data points to their unraveling. Tariffs, sanctions, interest-rate shocks, credit tightening, and “market discipline” are the emergency tools of a bloc that cannot maintain hegemony through consent. What the article presents as rational economic forecasting is, in reality, the ideological surface of a deeper geopolitical strategy: the attempt to preserve the triad’s shrinking command over a world sliding toward multipolarity.

This becomes clearest in the realm of global crisis displacement—where domestic economic instability is exported outward. When the U.S. raises interest rates to “fight inflation,” currencies collapse in West Africa. When Europe enforces austerity to “restore confidence,” hospitals and schools shutter across the continent. When Japan’s debt markets tremble, capital flees the Global South in search of “safe” assets. This outward push is not accidental; it is the logic of hyper-imperialism, the stage where internal contradictions of the imperial core are projected globally through finance, trade, sanctions, and monetary domination. It is no coincidence that the same article warning of bond-market fragility ignores the debt crises strangling dozens of African, Latin American, and West Asian economies. For the imperial core to appear stable, the periphery must absorb the disorder.

Even the AI boom, which Curr frames as both a miracle and a potential catastrophe, is more than a speculative bubble—it is the digital scaffolding of a technofascist order. The Digerati wing of the ruling class now builds economic strategy around data monopolies, algorithmic control, and automated surveillance. The Economist celebrates AI’s “wealth effects” without mentioning who owns that wealth or who labors beneath its shadow: the ghost workers labeling data; the warehouse hands monitored by real-time algorithms; the office staff whose keystrokes and break times are now indexed by machine. The AI boom is not a productive revolution but a financial and disciplinary one—an attempt to stabilize profitability through surveillance, layoffs, and speculative capital rather than wages or social investment. When this bubble bursts, it will not reveal a “confidence problem”—it will expose the artificial, engineered nature of U.S. economic resilience.

This is why the system appears to weather crisis: it does not solve crises; it redistributes them. Tariffs push instability onto trading partners. Interest-rate hikes push collapse onto debtor nations. Bond-market pressure pushes austerity onto workers and public institutions. AI speculation pushes insecurity onto the very people whose labor keeps society alive. And because this is a system built on unequal exchange, structural dependency, and coercive monetary regimes, the Global South absorbs the heaviest blows. Africa, Latin America, and West Asia are experiencing not incidental turbulence but the forced carrying of imperial crisis on their backs. The Economist’s “resilience” is nothing more than the imperial core cannibalizing its margins to buy itself another year.

A forecast that treats this as normal, temporary, or technical is not neutral analysis—it is ideological performance. When we reconnect the numbers to the people, regions, and classes they affect, the picture becomes unmistakable: a declining imperial system propped up by financial power, factional ruling-class struggle, digital surveillance, and the outward displacement of instability. This is the choreography of a world order cracking under its contradictions, seeking to maintain command not through prosperity but through force. And it is precisely in this widening gap—between the elite narrative and lived reality—that the possibility of a different future emerges. Not from predictions, but from struggle.

Building Power in the Belly of a Crisis Machine

If the story told by The Economist is one of technocrats bracing themselves for the next tremor, then the task before us is to stop living as spectators to their forecasts. A forecast is not a destiny. It is an ideological weapon—an instruction manual for how the ruling class intends to manage us through the crisis they created. So Section IV is not prophecy; it is a blueprint. It is the place where we translate the cold mechanics of Section II and the structural analysis of Section III into concrete action for people living inside the imperial core. This is about building power in the very spaces the forecast treats as passive terrain.

First, we confront tariffs and trade wars not as technical disputes, but as class offensives. When Trump’s tariffs raise prices on imports, the cost does not fall on the billionaire class—it falls on poor and working people, and on entire communities abroad who had no say in the matter. The antidote is not to politely argue for “smart trade” but to strengthen the movements already organizing against the machinery of economic coercion. The Debt Collective shows what this looks like on the domestic front: it builds power not through charity or pleading but through mass refusal, coordinated disruption, and a clear recognition that everyday people are already creditors to a system that feeds on their wages. Internationally, groups like Debt Justice and the Progressive International are stitching together a South–North coalition against austerity and the IMF’s chokehold. These are not think-tank experiments—they are training grounds for a generation learning to challenge the very debt architecture that The Economist treats as natural law.

Second, if central banks are the black boxes through which the ruling class governs wages, prices, and employment, then our task is to break that box open. The fight for monetary democracy can no longer be the niche hobby of policy wonks. The decisions made by the Federal Reserve shape everything from how much food you can buy to whether your city can afford clean water or your state can keep its teachers. Movements pressing for democratic oversight, worker-centered mandates, and climate accountability inside the Fed must be treated as part of the broader struggle for economic freedom. This means integrating Fed policy into labor campaigns, tenant organizing, and community assemblies—not leaving it in the hands of economists who think the “public” is the S&P 500.

Third, we confront the AI boom—not as a shiny miracle that might “fizzle” but as a battlefield where the front line is already drawn. Bosses see AI as a weapon to cut payrolls, intensify surveillance, pulverize job security, and expand their control over the rhythms of work. That is why unions across the country, from the AFL-CIO’s new AI initiative to the tech and telecom workers organizing under CWA and AWU-CWA, are demanding bargaining over how AI is deployed, expanding protections against layoffs, and fighting to expose the hidden labor—the “ghost workers” who label data, moderate abusive content, and stitch together the illusion of automation. This is one of the decisive organizing fronts of our time: either AI becomes another tool of extraction, or workers seize it as a terrain of struggle.

Fourth, the looming specter of austerity cannot be met with outrage alone. Bond markets are not gods, and their “discipline” is not a natural law; it is a political weapon. The 2022 British crisis showed how quickly a government can retreat under the threat of rising yields. The antidote is not to promise better management, but to build networks capable of resisting austerity before it arrives. Tenant unions, labor councils, climate coalitions, migrant justice organizations—these are the institutions that can block cuts, resist privatisation, and force governments to protect human needs over investor demands. The global End Austerity movement has already begun to connect these struggles. It is time for more people in the imperial core to join it not as sympathizers but as participants.

Finally, we must construct the intellectual and organizational infrastructure that the ruling class fears most: militant, working-class media and political education rooted in internationalism. Platforms like Weaponized Information exist not to comment on the news but to train people to intervene in it—to build cadre who can walk into their union hall or community meeting and explain, in clear terms, how tariffs, debt, interest rates, and AI speculation are all instruments in the same system of domination. This is the kind of knowledge the powerful rely on us never possessing. But once we grasp it, even at a basic level, the spell begins to break.

The truth is that the forces needed to dismantle the crisis machine are already alive: in the debtor strikes that rattle private lenders; in the organizing drives that challenge union-busting tech giants; in the rent-defense campaigns that refuse evictions; in the international alliances refusing austerity; in the new study circles where ordinary people learn to read the world critically and collectively. None of these movements appear in The Economist’s forecast—not because they are too small, but because they threaten to make the forecast irrelevant.

And that is the point. We are not here to “roll with the punches.” We are here to break the rhythm of a system that has turned the entire planet into its punching bag. The future will not be decided by the bond market, the Fed chair, or the next index of AI stocks. It will be decided by whether ordinary people, in the heart of the empire and across the world, organize their power fast enough to turn crisis into possibility. The Economist measures resilience by the survival of the system. We measure it by the survival—and liberation—of the people forced to live beneath it.

Leave a comment