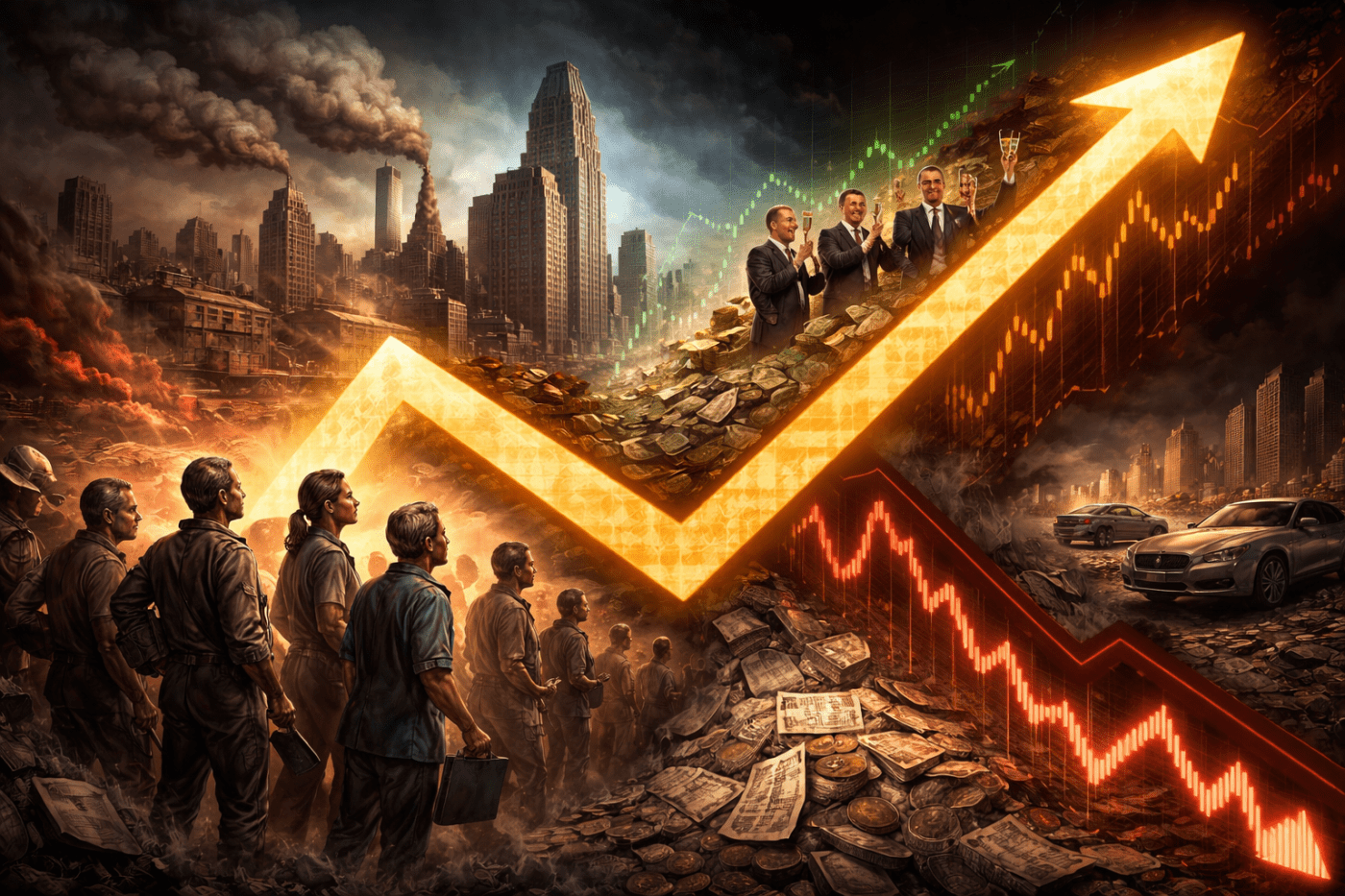

Wall Street calls it sentiment. Corporate media calls it divergence. But beneath the alphabet metaphors lies a decades-long transfer of wealth, power, and sovereignty from labor to capital. The numbers do not describe a mood swing. They describe a system working exactly as designed.

By Prince Kapone | Weaponized Information | February 11, 2026

When the Rich Describe the Poor, It Always Sounds Like “Confidence”

The target text for this excavation is Josh Tanenbaum’s Fortune commentary, “The economy isn’t K-shaped. For 87 million people, it’s desperate and for another 46 million it’s elite”, published on February 10, 2026 and syndicated through Yahoo Finance. On its surface, the piece performs a familiar corporate-media ritual: it admits the split, it names the pain, it gestures at volatility, and then it carefully walks the reader back to the safe side of the fence—away from power, away from causes, away from enemies. Its headline declares that the economy “isn’t K-shaped,” but the body reintroduces the same geometry with new labels: a “desperation economy,” an “elite economy,” and a fraying middle that threatens “stability.” The point is not to deny the split; the point is to translate the split into a managerial problem that can be handled without touching ownership, without confronting capital, and without recognizing class struggle as the real engine beneath the noise.

To understand what this text is doing, you start with where it’s written from. Tanenbaum is not writing from a shop floor, a warehouse, a hospital ward, or a tenant meeting where people compare eviction notices like baseball cards. His professional position is rooted in venture capital and the world of “solutions” designed for markets, employers, and investors—an ecosystem that tends to treat social breakdown as an opportunity for new products, new platforms, and new “tools.” Even his public profile reads like the résumé of someone trained to interpret workers as variables in a system rather than as a class with antagonistic interests. That orientation is not an insult; it is a location. It shapes what he can see, what he cannot name, and what he must keep off the table if he wants to stay intelligible to the people who sign checks. You can see that class location in plain sight through his own professional biography and affiliations, such as his listed role at Rebalance Capital.

The outlet matters just as much as the author. Fortune is not a neutral narrator hovering above the battlefield with a clipboard. It is business press—an instrument that exists to help the ruling class talk to itself, coordinate its anxieties, and discipline the public into accepting what capital needs next. Fortune’s ownership structure makes that orientation concrete. The magazine has reported its own sale and ownership arrangements, including the transition to billionaire ownership under Fortune Media Group Holdings, wholly owned by Chatchaval Jiaravanon, as described in Fortune’s own reporting on its ownership. This is not a conspiracy; it is the normal organization of ideological production under monopoly capital: the people who benefit from the system own the megaphones that explain the system.

With that institutional terrain established, we can excavate the narrative mechanics as they appear in the text itself—no “fact-checking” yet, no historical correction, no outside context injected like a sermon. The first move is a classic sleight-of-hand: the piece acknowledges material distress, then quickly relocates the central danger into the realm of psychology. “The most dangerous divergence,” we are told, “isn’t in wealth. It’s in confidence.” That sentence is the hinge on which the whole propaganda structure swings. It does two things at once. It admits that wealth divergence is obscene, while also implying that the real problem is what people believe about their situation, not the situation itself. In that frame, the crisis becomes a matter of perception and behavior, not ownership and power. The reader is guided away from asking “Who did this?” and toward asking “How do we restore belief?”

The second move is segmentation as pacification. The text does not speak in the blunt language of class, because class implies antagonism, and antagonism implies organization. Instead, it speaks in demographic containers—“87 million” here, “46 million” there—like a consultant’s slide deck. Once the working class is chopped into market categories, the struggle is no longer between labor and capital; it becomes a problem of “cohorts” with different “sensitivities.” That language does not simply describe reality; it disciplines the reader’s imagination. It trains the audience to see economic life as a set of consumer groups that need different interventions, rather than a class structure that demands confrontation.

A third technique is what we might call stability blackmail. The piece repeatedly frames the bottom half’s condition as a “stability risk,” warning that the danger is not the violence of deprivation itself, but what deprivation might do to the system’s smooth functioning. This is an old imperial reflex: the suffering of the many is tolerable until it threatens the comfort of the few. When the text describes a “Quiet Riot,” it is not honoring resistance; it is naming the nightmare of boardrooms—millions of people quietly withdrawing from the promises that keep the machine running. The poor are not presented as subjects with a program; they appear as a potential malfunction in the national operating system.

The fourth move is managerial ventriloquism. The piece leans on credentialed interpreters and “experts” to explain what people are feeling and why it matters, including the invocation of economist Peter Atwater’s emphasis on belief and control. The effect is subtle but decisive: the story becomes something that must be narrated by a professional class that is authorized to translate social pain into policy-safe language. Working people appear in the text largely as objects—data points, confidence readings, exposed households—not as speaking subjects with agency. The bottom arm of the economy is observed, diagnosed, and managed, but never allowed to author the meaning of its own condition.

The fifth technique is the softening of coercion into choice. The article describes the breaking point as “behavioral exit,” “opting out,” “stop optimizing,” “stop planning.” This is the language of consumer decision-making, not the language of compulsion. It makes structural constraint feel like personal preference. It quietly implies that the problem is that people are choosing badly—disengaging, withdrawing, losing faith—rather than recognizing that many are cornered into survival choices because the math no longer works. This rhetorical move is not a minor stylistic flourish. It is an ideological operation: it turns the system’s violence into the individual’s psychology.

A sixth move is solution funneling. After building the mood of danger—confidence collapse, recession signals, quiet instability—the text offers remedies that remain inside the same enclosure. “Wider participation,” “automatic wealth-building,” “reskilling,” “tools.” These are not presented as one possible lane among many; they are presented as the practical horizon itself. The reader is not invited to consider how power is organized in workplaces, how rents are extracted, how prices are set, how policy protects capital, or how collective struggle forces redistribution. The solutions are tailored to volatility only in the sense that they assume volatility is permanent and must be individually navigated, rather than politically abolished.

All of these devices work together to produce a single ideological effect: the piece acknowledges the fracture while neutralizing the politics that fracture should produce. It allows the reader to feel concern without arriving at blame, to recognize suffering without arriving at solidarity, and to sense danger without arriving at organization. The system is presented as “rigged” in a vague, atmospheric way, but the riggers remain unnamed, the rigging remains abstract, and the exit ramp leads not to struggle but to “tools” and “narratives.” In other words, the text performs the central function of corporate propaganda in a late-stage economy: it turns class war into risk management, and then asks the casualties to regain “confidence” in the very order that made them casualties.

From Confidence to Concentration: What the Numbers Actually Say

In Part I we dismantled the framing. Now we deal in measurements. The Fortune commentary cites falling consumer confidence, 87 million people living at or below roughly 200% of the federal poverty level, 46 million earning $100,000 or more, stock ownership concentrated at the top, and consumption powered disproportionately by higher earners. Those claims can be verified. But verification is only the beginning. When placed in full historical and structural context, they reveal not a mood swing—but a long-engineered redistribution of income, assets, and power.

Start with sentiment. The Conference Board Consumer Confidence Index confirms that expectations have dipped into territory historically associated with recessionary conditions. People are anxious. But sentiment indicators measure perception, not structure. They tell us how households feel inside an economic architecture whose ownership patterns remain unchanged.

The segmentation cited in the article aligns with official data. The U.S. Census Bureau’s poverty reports show tens of millions of Americans living at or near fragile income thresholds. Meanwhile, the IRS Statistics of Income tables demonstrate that households earning above $100,000 represent a minority of filers yet capture a disproportionate share of total national income. The split is real. But counting the segments does not explain why the split persists across decades.

Ownership is where the structure sharpens. The Federal Reserve’s Distributional Financial Accounts show that the top 10% of households hold the overwhelming majority of corporate equities and mutual fund shares. Within that group, the top 1% alone control roughly half of all directly and indirectly held equities. This means that stock market gains overwhelmingly benefit a narrow class of asset holders. When headlines declare that “the economy is strong” because markets are rising, they are describing the prosperity of those who own the market—not the condition of wage earners broadly.

Consumption patterns confirm this divergence. The Bank of America Institute’s analysis of consumer spending documents widening gaps, with upper-income households accounting for a disproportionate share of recent consumption growth. Research from the Minneapolis Federal Reserve shows that post-pandemic wage convergence slowed, with lower-income wage gains cooling relative to higher brackets. Growth at the top masks stagnation below.

The longer arc becomes visible when we examine labor’s share of national income. Data series available through FRED – Labor Share of Income reveal a secular decline in labor’s portion of GDP relative to corporate profits over the past several decades. As productivity has risen, a smaller proportion of national output has flowed back to workers in the form of wages and salaries. This is redistribution by structure, not by accident.

Corporate profits tell the complementary story. The Bureau of Economic Analysis reports profits near historical highs as a share of GDP in recent years. At the same time, the International Monetary Fund has documented rising markups among dominant firms over recent decades, indicating increased pricing power and concentration. Higher markups combined with concentrated ownership intensify upward distribution.

Household balance sheets show the consequences. The Federal Reserve Bank of New York’s Household Debt and Credit Report indicates total household debt exceeding $18 trillion, with elevated credit card balances and rising delinquency transitions in auto and consumer loans. When wage growth lags behind housing, healthcare, and insurance costs, households rely on credit to maintain consumption. What appears as a “confidence problem” often corresponds to debt dependence.

This domestic configuration sits within a wider global structure. The UNCTAD Trade and Development Report 2024 warns of subdued global growth and persistent inequality between and within nations. The World Inequality Report documents the long-term concentration of income and wealth globally, with top deciles capturing a dominant share of gains since 1980. U.S. asset markets operate at the apex of a system characterized by uneven exchange and capital concentration. Capital inflows during global turbulence reinforce asset values at the center while peripheral economies face higher borrowing costs and instability.

Technological restructuring compounds these dynamics. Research from Brookings on automation and artificial intelligence indicates that a substantial share of U.S. workers face significant task exposure. The OECD’s studies on digitalization similarly highlight uneven labor-market effects. Productivity growth does not automatically produce wage growth; distribution depends on institutional power and ownership structure.

When these strands are woven together—concentrated asset ownership, declining labor share, elevated corporate profits, widening consumption gaps, mounting household debt, global inequality, and automation exposure—the divergence described in the Fortune article ceases to resemble a temporary psychological imbalance. It reflects a material reorganization of income, ownership, and institutional power decades in the making. Confidence fluctuates. Asset concentration does not fluctuate nearly as easily. The “K-shaped” divergence rests on structural foundations that extend far beyond the latest survey reading.

When the Split Stops Being a Chart and Starts Being a System

Once you line the numbers up honestly, the letter disappears. The “K” stops being a clever visual and starts looking like a blueprint. What Fortune describes as a split between the “desperate” and the “elite” is not a mood disorder in the national psyche. It is the mature stage of a system that has learned how to grow upward while hollowing out the ground beneath it. The data from Part II—shrinking labor share, swollen corporate profits, extreme asset concentration, widening consumption gaps, rising household debt—are not random fluctuations. They are the anatomy of monopoly-finance capital doing exactly what it has been designed to do: concentrate surplus and socialize risk.

Start with the most basic contradiction. Workers produce more per hour than previous generations could have imagined. Productivity rises. Technology accelerates. Yet labor’s share of national income declines. That means the slice going back to the people who generate the value gets thinner, while the slice flowing upward to corporate profits and financial returns grows fatter. That is not an emotional event. It is arithmetic. The surplus does not vanish; it is absorbed elsewhere. And in our era, it is absorbed primarily through financial channels—stocks, buybacks, dividends, asset inflation. The upward arm of the K is not powered by a broad flowering of prosperity. It is powered by financial consolidation.

When asset ownership is concentrated at the top, stock market booms are not national celebrations. They are class celebrations. A rising index does not lift all boats; it inflates the yachts. So when business media says the economy is strong because equities are strong, it is speaking from a specific balcony. From below, the view looks different: rising rents, debt balances creeping upward, wages that no longer stretch to the end of the month. The so-called “confidence gap” begins to look less like psychology and more like class position.

This internal divergence is not sealed within national borders. It sits inside a global order structured by unequal exchange. Capital headquartered in the imperial core extracts value from labor across the Global South through supply chains, intellectual property regimes, and dollar dominance. The concentration of wealth in the United States is intertwined with wage suppression and volatility elsewhere. The K inside the core mirrors the K across the world system. The top floats because value flows toward it—from logistics corridors, factories, plantations, and mines that remain largely invisible in corporate commentary.

At home, the mechanism tightens. Automation expands. Digital platforms reorganize work. Productivity gains do not translate into broad wage gains because institutional power—union density, bargaining leverage, democratic control over investment—has been eroded for decades. When wages lag behind the cost of living, debt fills the space. Households borrow to maintain the illusion of normalcy. Credit cards become shock absorbers for a system that refuses to distribute gains equitably. The bottom half of the K is not suffering from a lack of optimism; it is trapped inside a balance-sheet reality.

What emerges from this configuration is internal uneven development. Historically, uneven development described the gap between industrial cores and exploited peripheries. Now that logic is reproduced within the core itself. Asset owners experience compounding returns and portfolio anxiety. Working-class communities experience wage stagnation, debt stress, and exposure to automation. The periphery is no longer only abroad; it is in rural counties, deindustrialized towns, warehouse belts, and urban neighborhoods where capital extracts value without reinvesting stability.

When broad material integration weakens, governance adapts. A society that once relied on rising living standards to secure consent must find other methods when those standards plateau or decline. The language of “confidence” becomes useful here. It reframes structural contradiction as emotional turbulence. It suggests that what needs repair is belief, not distribution. That move is not accidental. It stabilizes the order by shifting attention away from ownership and toward psychology. If people just regain faith, the story goes, the machine will hum again.

But machines do not hum on faith. They hum on power. When the top decile controls the overwhelming majority of financial assets while the bottom half juggles debt and insecure employment, the system is governed through asymmetry. Gains accumulate upward. Risks cascade downward. Volatility means portfolio fluctuations for some and eviction notices for others. That is not a temporary imbalance; it is a design feature of a system that prioritizes financial returns over social stability.

In a multipolar world where global dominance is contested, these pressures intensify. Capital seeks secure supply chains, resilient asset bases, and disciplined labor markets. Automation becomes not only a productivity tool but a control mechanism. Elevated markups signal growing monopoly power. Financial markets become reservoirs for surplus that cannot be profitably absorbed through broad-based employment expansion. Under these conditions, divergence is not an accident. It is the rational outcome of strategic priorities.

From the standpoint of the global working class and peasantry, the picture sharpens further. Workers in the core face declining labor shares and mounting debt. Workers in the periphery face suppressed wages and exposure to volatile capital flows. Different geographies, same circuit. The system extracts value across borders and concentrates it upward. The K is not simply an American letter. It is the signature of a world economy organized around accumulation at the top and managed precarity below.

What mainstream commentary calls “instability” is in fact contradiction. The contradiction between rising productivity and stagnant wages. The contradiction between asset inflation and household insecurity. The contradiction between global rent extraction and domestic stagnation. These contradictions cannot be resolved through renewed optimism. They require transformation in ownership, distribution, and institutional power. Without that, the split will not heal. It will harden.

So the K-shaped economy is not a passing distortion or a quirk of post-pandemic adjustment. It is the visible geometry of a system that has shifted from expansion to consolidation. Surplus concentrates. Labor fragments. Finance dominates. And political authority adjusts to manage the fallout. The question is no longer whether the split exists. The question is what forces will organize around it—and to what end.

From Fracture to Frontline: Organizing the Many Against the Few

If the K is a structure, then it is also a signal. It tells us where power is pooled and where pressure is building. The upward arm concentrates ownership, profits, and political influence. The downward arm concentrates debt, insecurity, and anger. The ruling class reads this configuration as a management problem—how to contain discontent without redistributing power. The working class must read it differently: as an organizing map.

Across the United States, the outlines of resistance are already visible. Warehouse workers, nurses, educators, and logistics workers have rebuilt strike capacity in sectors once declared permanently subdued. The recent wave of union drives at companies like Amazon and Starbucks—imperfect, uneven, but real—signals a refusal to accept a world where corporate profits soar while paychecks stagnate. Tenant unions in cities from Los Angeles to Kansas City have organized rent strikes and eviction defenses, confronting the asset logic that treats housing as a speculative instrument rather than a human need. These struggles are not abstract. They are direct responses to the material conditions described in Parts II and III.

Beyond the workplace and the rent ledger, community-based formations have grown in response to widening precarity. Mutual aid networks that emerged during the pandemic did not dissolve; many have evolved into durable infrastructures—food distribution programs, childcare collectives, transportation support systems. In regions hit hard by deindustrialization and automation exposure, worker centers have provided legal support, wage theft documentation, and political education. These formations are modest compared to the scale of capital concentration, but they represent the seeds of counter-power rooted in lived experience.

Internationally, the connection becomes clearer. Farmers’ movements in India that challenged corporate agricultural restructuring, anti-austerity coalitions in Latin America resisting debt discipline, and labor federations in Africa organizing against price shocks are confronting different expressions of the same surplus-extraction logic. As multipolar alignments deepen through formations like BRICS+, governments in the Global South are exploring alternatives to dollar-denominated dependency and external financial discipline. These shifts are not revolutionary by default, but they open space. And space is what movements need to breathe.

For those inside the imperial core, the task is to align with these currents rather than retreat into nationalist fragmentation. Concrete action begins with identifying the institutions that sit at the apex of the K. Organize campaigns that expose corporate ownership webs. Pressure pension funds and public institutions to divest from firms engaged in predatory pricing, union suppression, and speculative housing practices. Support strike funds and solidarity networks that extend beyond individual workplaces. Build rank-and-file committees that link sectors—logistics to retail, healthcare to education—so that disruption is coordinated rather than isolated.

Digital terrain is another front. Map rent increases and wage stagnation in real time. Document corporate price hikes and executive compensation packages. Create open-access databases that trace who owns what and who profits from which decision. When information is weaponized upward, transparency becomes a tool downward. Proletarian cyber resistance does not require exotic technology; it requires disciplined documentation and coordinated dissemination.

Political education remains decisive. Study groups anchored in working-class neighborhoods, union halls, and community centers can transform isolated frustration into collective clarity. Connect the decline in labor share to local plant closures. Connect asset concentration to rent hikes. Connect global supply chains to local job insecurity. When people see the structure, they stop blaming themselves and start questioning the architecture.

None of this unfolds automatically. The top of the K will not surrender its position because the data look obscene. But history shows that concentrated power invites concentrated resistance. The same contradictions that harden inequality also create the conditions for solidarity—across race, region, and nationality. The worker in a warehouse in Ohio and the farmer resisting debt in Punjab confront different faces of the same order. The tenant facing eviction and the gig worker juggling three apps are bound by a shared precarity.

The fracture of the K is not destiny. It is a battlefield. The question is whether those on the lower arm remain dispersed silhouettes or become organized subjects. When isolation turns into coordination, when despair turns into disciplined strategy, the geometry changes. What was once a letter becomes a line of struggle.

Leave a comment